The “convenience of the employer” rule is one of those policies that quietly shapes paychecks, compliance, and even take-home income.

It’s a regulation designed decades before remote work became mainstream, yet today it touches thousands of professionals working from outside their employer’s state.

For HR managers and payroll teams, it’s a compliance maze. For employees, it’s often an unwelcome surprise at tax season.

The stakes are high: get it wrong, and you risk double taxation.

Get it right, and you help create clarity, predictability, and fairness in a remote-first workforce.

So, how exactly does this rule work—and why should remote teams pay attention?

What Is the Convenience of the Employer Rule?

The convenience of the employer rule is a tax regulation applied by certain U.S. states. It says that if an employee works remotely outside the employer’s state, those workdays may still count as taxable in the employer’s state unless the work is required there for business reasons.

This means remote workers can end up owing taxes in two states even though they only live and work in one. Understanding this rule is key for both employees and HR teams, as it directly affects payroll, withholding, and compliance.

Definition and Legal Background

The rule dates back decades, originally built to protect states from losing tax revenue when employees worked outside their borders. At its core, the law determines where income is sourced for tax purposes. If the employee is working remotely purely for personal convenience, the employer’s state still claims taxation rights.

Over time, legal cases have shaped its interpretation, but the principle remains: states with this rule prioritize their tax jurisdiction over where the employee physically works.

Why Employers Apply the Rule?

Employers follow the convenience of the employer rule because they are legally required to withhold income taxes in the states that enforce it. The alternative would be penalties, audits, and payroll disputes. In practice, this creates a compliance-heavy workload for HR teams, who must track employee work locations and justify them under the rule.

For employers, it’s less about choice and more about risk management, ensuring payroll systems meet the demands of multiple state tax authorities.

How the Rule Shapes Remote Work Experience?

The rule shapes remote workers’ financial realities by influencing where their income is taxed. For many, this can result in double taxation—paying in both their home state and their employer’s state. It also limits flexibility: employees may hesitate to work remotely from another state for fear of unexpected tax bills.

For HR and payroll managers, the rule adds another layer of complexity to an already evolving remote work structure, requiring ongoing education and proactive communication.

Tax Obligations and the Risk of Double Taxation

Double taxation occurs when both the employee’s home state and the employer’s state enforce income tax on the same earnings. While some states offer credits to reduce the burden, others don’t, leaving workers at risk of paying more than their fair share.

According to the Tax Foundation, around 70% of remote workers reported confusion about multi-state tax obligations in 2025. This confusion highlights why both workers and HR managers need clarity before tax season arrives.

Payroll and Withholding Challenges for HR Teams

For HR and payroll managers, the convenience of the employer rule complicates payroll systems. Employers must determine where to withhold taxes, keep records of employee work locations, and maintain compliance with overlapping state laws. A single misstep can result in penalties or employee frustration.

To keep operations smooth, payroll teams often need specialized software, tax advisors, or in-house compliance processes—resources that may be especially costly for smaller organizations navigating remote work expansion.

States That Enforce the Convenience of the Employer Rule

Not every state applies the convenience of the employer rule, but those that do often create the most confusion for payroll and employees. These states claim tax rights even when work is performed elsewhere, unless the employee can show that the location is required for business.

For HR managers, knowing which states enforce the rule is crucial to preventing errors in withholding and payroll reporting. For employees, it determines where income is taxed and whether they face the risk of double taxation.

Oregon

Oregon applies this rule by taxing employees who work remotely outside the state if the work is performed for their own convenience rather than the employer’s necessity. Remote employees tied to Oregon-based companies must track business-related reasons for working elsewhere to avoid extra taxation.

Delaware

Delaware enforces this rule to preserve state tax revenue. Employees working remotely outside Delaware are still subject to Delaware income tax unless they can show their employer requires them to work elsewhere. This makes employer documentation critical.

Pennsylvania

Pennsylvania applies the rule but offers exceptions through its reciprocal agreements with certain neighboring states. Remote employees who live outside Pennsylvania should review whether their state has a reciprocity arrangement to reduce the risk of double taxation.

Alabama

Alabama has adopted its own version of the rule, taxing remote employees who work outside state borders unless the work is performed out of business necessity. Employers must carefully classify remote work to remain compliant.

New Jersey

New Jersey enforces the rule as a defensive measure against neighboring states. Employees working for New Jersey companies may owe state income taxes even while living and working elsewhere, unless their duties require out-of-state work.

New York

New York is the most well-known enforcer of this rule. Employees working remotely outside the state for convenience are taxed as though they were working in New York. With strict enforcement and extensive case history, New York sets much of the precedent for this policy.

Nebraska

Nebraska applies the rule to protect its tax base. Employees of Nebraska companies working from other states for personal convenience are subject to Nebraska taxation. Proper documentation of employer-required duties outside the state is essential.

Connecticut

Connecticut enforces the rule and follows a model similar to New York’s. Unless the employer directs work to be performed elsewhere, Connecticut claims taxation on all wages earned by employees tied to Connecticut-based companies, regardless of where they perform the work.

Comparison of States That Apply the Rule

Pros and Cons for Remote Employees

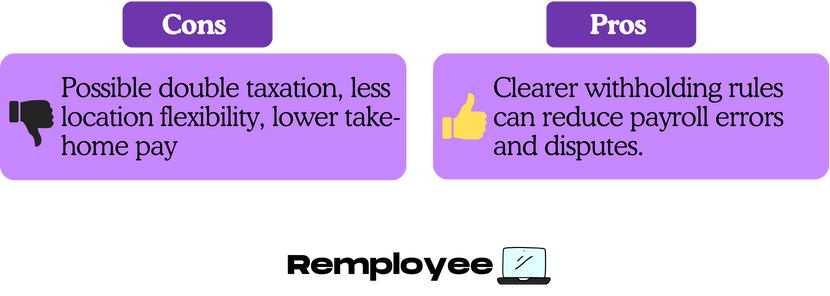

The rule brings both drawbacks and advantages, depending on circumstances.

- Cons: Risk of double taxation, limited flexibility to choose work location, and potential for lower take-home pay.

- Pros: In certain cases, clear guidelines can simplify withholding for employers, reducing disputes or payroll errors.

For employees, the downsides often outweigh the benefits, particularly if their home state doesn’t grant credits against taxes paid to another state. For HR leaders, explaining both sides ensures transparency during hiring and onboarding.

Legal Cases and Precedents Shaping the Rule

Court rulings have shaped how the convenience of the employer rule is applied. For instance, challenges in New York and Connecticut have repeatedly upheld the state’s authority to tax income earned outside its borders.

These cases confirm that unless federal law changes, the rule remains enforceable. HR managers need to be aware of such precedents because they limit negotiation options and set the boundaries for compliance. Employers who ignore legal history may expose their organizations to liability and disputes.

Strategies Remote Workers Can Use to Navigate the Rule

Remote employees can adopt strategies to reduce the burden of this rule:

These strategies help employees stay prepared and reduce the financial impact of overlapping tax obligations.

Tax Planning Tips for Employees and Employers

Effective planning reduces surprises during tax season. Employees should document their remote work arrangements in writing and review their state’s reciprocity agreements. Employers, on the other hand, benefit from proactive payroll audits and cross-state compliance checks.

Collaboration is key: HR managers and employees should communicate early about potential risks. By investing in tax planning, both sides avoid last-minute disputes, unexpected bills, and compliance penalties that can hurt relationships and trust.

Employer Negotiation Options and Available Tools

Employers can negotiate terms with remote workers to ease tax burdens, such as defining work locations for business necessity or offering tax equalization benefits. Tools like ADP SmartCompliance simplify these processes by automating multi-state payroll compliance, tracking tax credits, and reducing errors.

While no tool eliminates the rule itself, using technology helps HR teams manage the complexity more efficiently, ensuring fair treatment for employees while keeping organizations compliant.

Alternatives and Policy Debates Around Remote Work Taxation

Debate continues around whether the convenience of the employer rule should remain in place. Critics argue it penalizes remote workers and limits flexibility, while states defend it as necessary for revenue protection. Proposals in

Congress have called for clearer, nationwide remote work taxation policies to prevent double taxation, though progress has been slow. Until reforms are made, both employees and HR leaders must work within current rules while advocating for fairer alternatives in the future.

What Remote Workers Need to Know About the Rule

The convenience of the employer rule may feel outdated, but it remains powerful in shaping the lives of remote employees. It determines where income is taxed, whether payroll stays compliant, and how much employees keep at the end of the year.

For HR leaders, clear communication and compliance processes are essential. For employees, careful planning and proactive documentation make all the difference. Knowing how the rule works turns confusion into control and keeps remote work sustainable.

Ben doesn’t buy into “the way it’s always been done.” He’s spent his career challenging hiring norms and rethinking how remote work should feel. At Remployee, he helps create honest tools and opportunities for people tired of the gig economy’s empty promises.